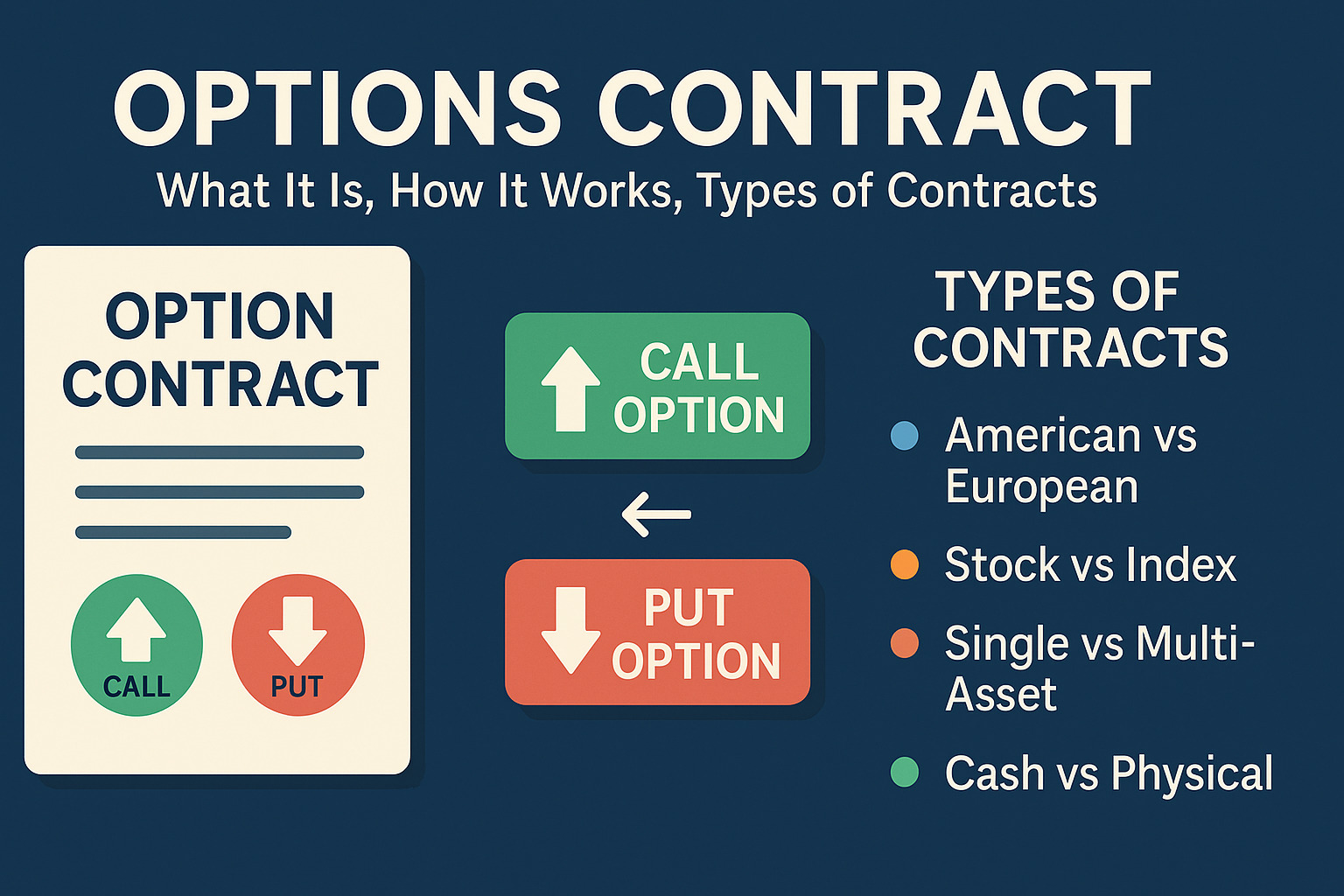

Options Contract: What It Is, How It Works, Types of Contracts

An options contract is a financial agreement that gives the buyer the right—but not the obligation—to buy or sell an asset at a specific price by a certain date. Calls are used to profit from price increases, and puts from price declines, while the premium paid defines the buyer’s risk.

Options trading has surged by nearly 150% over the last decade. Retail investors now account for over 40% of all trades.

Many are drawn to options because they offer control over large stock positions at a lower cost. This makes them a powerful tool for both beginners and pros.

An option contract gives you the right—not the obligation—to buy or sell an asset at a set price. Each standard contract covers 100 shares of stock.

There are two main types: calls (to buy) and puts (to sell). The premium you pay is your maximum loss when buying options, no matter how the stock moves.

This guide covers the essentials of options contracts from start to finish. You’ll get clear definitions, real examples, and advanced strategies to match your trading goals.

- Options contracts grant the right—but not obligation—to buy (calls) or sell (puts) an asset at a set price before expiration.

- Standard contracts typically control 100 shares; core components include strike price, expiration date, and premium.

- Calls benefit from rising prices; puts benefit from falling prices—buyers risk only the premium, sellers face greater risk.

- Strategies range from simple (long calls/puts, covered calls) to advanced (spreads, straddles, iron condors, calendar spreads).

- Risk management hinges on position sizing, Greek monitoring, and disciplined exits to protect capital.

What Is an Option Contract: Core Definition and Purpose

Option contracts create a binding legal agreement between two parties. The buyer gets the right—but not the obligation—to buy or sell an underlying asset at a set price within a specific timeframe. These flexible financial instruments help with hedging against market changes, income generation, and they let investors control larger positions with minimal capital.

Legal Structure of Options Contracts

Option contracts create different commitments for each party. The seller (or writer) makes a legally binding promise to keep an offer open for a set time and gets paid for this promise. Contract law principles require this payment to make the agreement valid in most jurisdictions. Breaking this commitment leads to a contract breach. The options on assets like land need registration to bind third parties.

Key Components: Strike Price, Expiration Date, and Premium

Every option contract has three basic elements:

- Strike Price: The set price where you can buy or sell the underlying asset if you exercise the option. This price shows if an option is in-the-money (ITM), at-the-money (ATM), or out-of-the-money (OTM).

- Expiration Date: The last day you can exercise the option. The contract ends after this date, which makes options time-dependent instruments.

- Premium: The buyer pays this amount upfront to the seller. Several factors affect this price:

- The option’s moneyness (how the strike price relates to current market price)

- Time left until expiration

- Market volatility

The Rights vs. Obligations Difference

The difference between rights and obligations stands out as the most crucial aspect of options. Buyers get rights without obligations—they choose if they want to exercise the contract. Sellers take on obligations without rights—they must act if the buyer exercises. This creates very different risk profiles. Buyers can only lose their premium, but sellers might face big losses if the market moves against them.

Types of Options Contracts in Financial Markets

Options contracts come in different categories based on their rights and exercise methods. You need to understand these basic differences to make options trading work.

Call Options: The Right to Buy

Call options give holders the right—without obligation—to buy an underlying asset at a specified strike price before the expiration date. We used these options when prices were expected to rise, and their value increases as the underlying security’s price goes up. You can calculate the breakeven point by adding the strike price and premium paid. Investors choose calls to make use of information about market exposure, since the premium is just a fraction of the underlying asset’s price.

Put Options: The Right to Sell

Put options work differently from calls. They give you the right—without obligation—to sell an underlying asset at the strike price before expiration. The value of puts goes up when the underlying security’s price drops. You get the breakeven point by subtracting the premium from the strike price. Traders use puts to speculate on predicted price drops and protect their existing investments.

American vs. European Exercise Styles

Your option rights depend on the exercise style. American-style options let you exercise any time before expiration, which gives you the most flexibility. European-style options only allow exercise at expiration. Stock and ETF options usually follow the American style, while broad-based equity indices use European-style options. This difference affects option prices. American options cost more than similar European options because they offer more exercise flexibility.

Standard vs. Non-standard Contract Specifications

Standard options contracts usually represent 100 shares of the underlying asset. Corporate actions like stock splits, mergers, or special dividends can create non-standard options with different specifications. These adjusted contracts keep things fair between option buyers and sellers after major corporate events. Non-standard options usually have unusual deliverables, less liquidity, and special settlement terms. They help maintain the original contract’s economic value despite changes in the underlying asset.

How Options Contracts Work in Practice

Becoming skilled at trading options starts with understanding how they work. Learning these practical elements will help you confidently direct your way through options markets.

The Options Chain: Reading Contract Information

Option chains display all available contracts for a particular security. These tables show calls on the left and puts on the right, with strike prices in the middle. They provide substantial trading information. Most platforms use color codes—green highlights in-the-money options while red shows out-of-the-money positions. Each row shows key data: contract symbol, last price, bid/ask spread, volume, and open interest. A detailed look at these elements helps you spot opportunities based on liquidity and market sentiment.

Contract Multipliers and Deliverables

Standard equity options use a contract multiplier of 100, which means each contract controls 100 shares of the underlying stock. The premium shows as a per-share price—for example, $2.50—but your actual cost is $250 per contract ($2.50 × 100). Stock splits or mergers can create non-standard options that have different multipliers or unique deliverables. These adjusted contracts might include varying share quantities, cash components, or debt participations.

Exercise and Assignment Process

The option exercise creates a ripple effect through financial intermediaries. Your broker alerts the Options Clearing Corporation (OCC) after you exercise, and the OCC randomly assigns the obligation to a seller. Call option exercise means buying shares at the strike price, while put exercise means selling shares. In-the-money options at expiration automatically exercise unless you specifically say otherwise.

Options Settlement Methods

Stock and ETF options typically use physical settlement, which involves actual delivery of the underlying security. Index options usually use cash settlement, where only the monetary difference between strike and market price changes hands. American-style options let you exercise anytime before expiration, while European-style options restrict exercise to expiration only. This difference shapes both risk management and trading strategies, particularly regarding overnight market movement risks.

Options Pricing Mechanics and Valuation

Options pricing knowledge helps traders make better decisions. The premium you pay or receive for an option contract depends on several components and mathematical models.

Intrinsic vs. Time Value Components

Every option premium has two main parts: intrinsic value and time value. The intrinsic value shows what an option would be worth if you exercised it right now. Call options calculate this as the underlying price minus strike price (when positive). Put options use strike price minus underlying price (when positive). Options that lack intrinsic value are “out of the money.”

Time value makes up the rest of the premium beyond intrinsic value. This reflects the chance that the option could become more valuable before it expires. Time value drops as the expiration date gets closer – we call this time decay. The decay pattern isn’t linear. The option loses about one-third of its value in the first half of its life and two-thirds in the second half.

The Greeks: Delta, Gamma, Theta, Vega, and Rho

Traders use “Greeks” to measure different types of risk:

- Delta (0 to 1 for calls, 0 to -1 for puts): Shows how much an option’s price moves when the underlying asset changes by $1.

- Gamma: Tells you how fast delta changes with underlying price movement.

- Theta: Measures daily value loss from time decay.

- Vega: Shows how sensitive the option is to volatility changes.

- Rho: Reveals how interest rate changes affect the option.

Black-Scholes Model Fundamentals

The Black-Scholes model came out in 1973 and created a mathematical framework to price options. It needs five inputs: current stock price, strike price, time until expiration, risk-free interest rate, and volatility. The model is accessible to more people now but has its limits. It assumes European-style exercise and constant volatility. In spite of that, it remains the foundation for most options pricing calculations and helps traders figure out theoretical values for complex positions.

Real-World Option Contract Examples

Real-life examples help us learn about option contracts and show how they work in different market situations.

Stock Option Contract Example with Profit/Loss Calculation

A plastic manufacturer’s story shows how options work in practice. The company worried about oil prices that sat at $25 per barrel. They feared prices might go above $30, so they bought a call option with a $30 strike price for a $1 premium. The manufacturer would only lose the $1 premium if oil prices stayed below $30. When prices jumped to $33, they used the option to buy at $30. This saved them $2 per barrel after counting the premium ($33 – $30 – $1). Their smart hedge limited losses while keeping the chance for bigger gains.

Index Option Contract Specifications

S&P 500 index options (SPX) use a $100 multiplier, which means each contract equals $100 times the index value. Strike prices come in steps of $5, $10, $25, $50, $100, and $200 based on when they expire. Nasdaq-100 index options (NDX) also use the $100 multiplier but work a bit differently. Their exercise prices come in $5 steps for contracts under $3 and $10 steps for those above. Both types follow European-style exercise rules, which only allow execution when they expire.

ETF Options Contract Case Study

Long-term equity anticipation securities (LEAPS) on defensive sector ETFs can diversify a tech-heavy portfolio. Investors cut their concentration risk by putting 25% of their funds into options on utilities, real estate, treasuries, and gold ETFs. This needed minimal capital. They picked options with 0.80 delta and January 2026 expiration to balance leverage and time decay effectively.

Commodity Options Contract Structure

Commodity futures options let you buy or sell specific futures contracts. Take a crude oil producer who wants protection from falling prices. They might buy a $60 put option to set a price floor. The option gets exercised if prices drop below $60. Higher prices mean they just lose the premium. Time plays a crucial role here – these options lose value as they get closer to expiration.

Call Options Strategies for Bullish Markets

Bullish options strategies let you profit from rising markets and adjust your risk exposure based on your investment goals. You can choose from aggressive leverage plays to conservative income-generating techniques.

Long Call Strategy: Maximum Leverage with Defined Risk

A call option purchase gives you substantial leverage with clear risk limits. You get the right to buy shares at the strike price until expiration by paying just a fraction of the stock’s cost. Your risk stays limited to the premium paid plus commissions, while your profits can grow unlimited as the stock price rises. You break even at the strike price plus the premium paid. To name just one example, a stock at $37.50 with a $38 call bought for $1 would break even at $39.

Covered Call Writing for Income Generation

This approach combines holding stock and selling call options against your shares. We used this strategy in neutral to slightly bullish markets to create income through premium collection. The premium helps protect against moderate price drops, but caps your gains if the stock climbs above the strike price. This strategy works best when stocks stay relatively stable or show modest gains.

Bull Call Spread: Balancing Cost and Potential Return

A bull call spread combines buying a lower-strike call while selling a higher-strike call with similar expiration dates. This strategy:

- Cuts your original investment compared to buying just the lower strike call

- Caps maximum profit at the difference between strike prices minus the net cost

- Creates a defined risk equal to the net debit paid for the spread

You break even at the lower strike price plus the net premium paid.

LEAPS Calls for Long-Term Market Exposure

LEAPS (Long-Term Equity Anticipation Securities) are options that expire beyond one year—sometimes lasting up to three years. These long-duration calls help you benefit from potential long-term price gains while using less capital than buying stocks outright. Yes, it is advantageous for investors who want extended exposure to quality companies without the full upfront cost of share ownership.

Put Options Techniques for Bearish and Protective Positions

Put options give you strategic advantages as markets trend downward or you need protection against potential losses. These contracts let you sell assets at preset prices. This creates great opportunities to speculate and manage risk, unlike call options.

Long Put Strategy: Profiting from Market Declines

Buying put options gives you exposure to downward price movements with clear risk limits if you expect stock prices to fall. A put contract gives you the right to sell the underlying asset at the strike price until it expires. You won’t lose more than the premium and commissions you paid. Your profits could grow until the underlying hits zero. You can find your breakeven point by subtracting the premium from the strike price. Let’s say you buy a $100 strike put for $3.15 – your breakeven would be $96.85.

Put values change based on their delta, which is usually -0.50 for at-the-money options. A $1.00 drop in the stock price typically makes the put worth $0.50 more. Your timing needs to be right because puts lose value over time, especially near expiration.

Protective Puts for Portfolio Insurance

As with home insurance, protective puts create a price floor for your stocks. You create a safety net by buying puts against stocks you own while keeping the chance to profit if prices rise. This works well if you’re bullish long-term but worried about short-term risks.

You’ll know your maximum risk during the put’s life, and you’ll have more flexibility than stop-loss orders. These puts let you consider your choices instead of selling automatically when prices drop. The biggest drawback is that you’ll pay more in total investment costs due to the premium.

Bear Put Spread: Optimizing Downside Exposure

Bear put spreads can cut your costs instead of just buying puts. You buy a higher-strike put and sell a lower-strike put that expires on the same day. This reduces your original investment but limits potential gains.

Bear put spreads work best if you expect modest price drops. This strategy helps you use your capital efficiently if you think the stock will fall to the lower strike price but not much further. Your maximum profit is the difference between strike prices minus what you paid. Your risk stays limited to your original investment.

Advanced Multi-Contract Options Strategies

Advanced traders go beyond simple single-contract plays. They combine multiple options to create positions that zero in on specific market conditions. These multi-leg strategies give you specialized risk-reward profiles that match different market expectations.

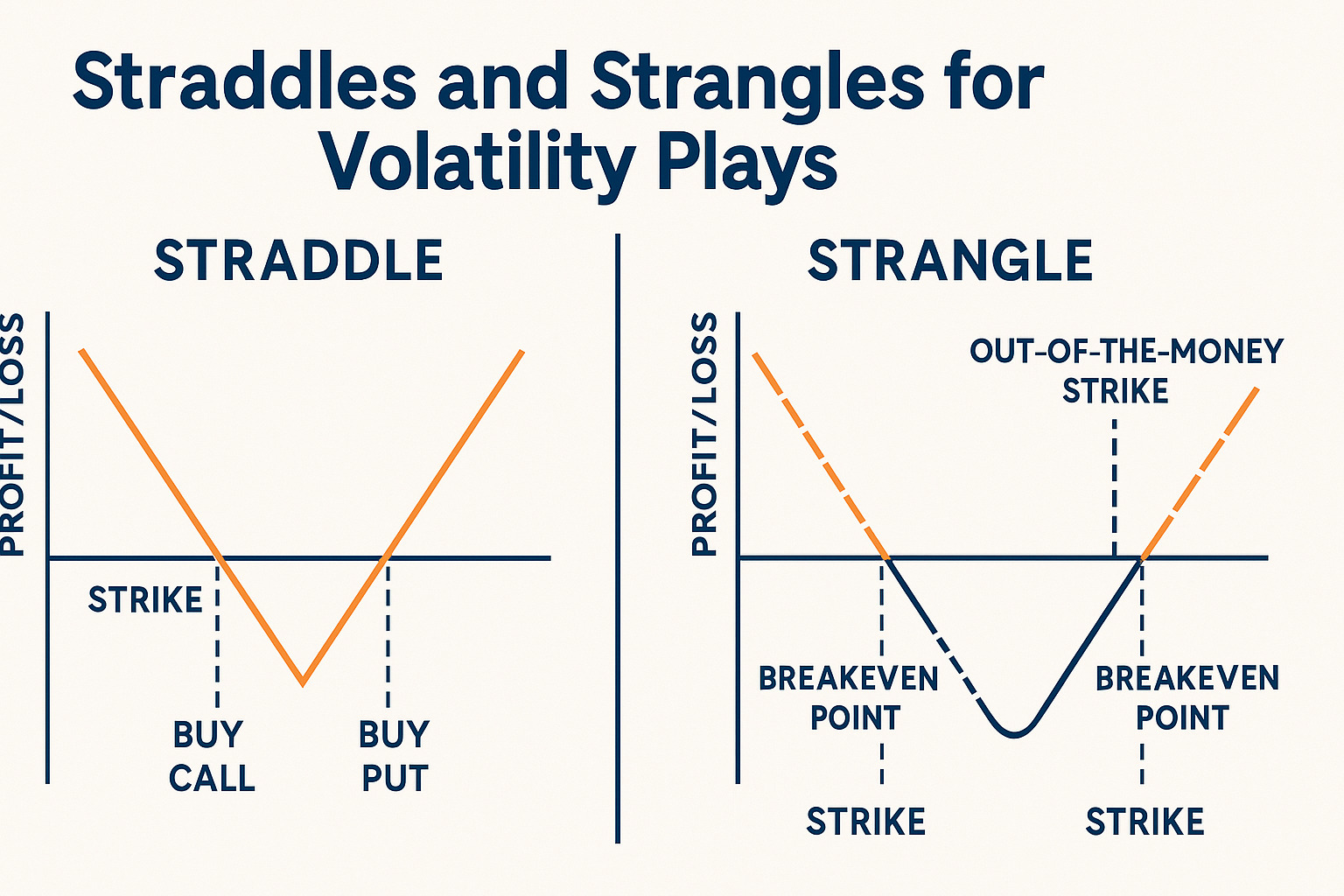

Straddles and Strangles for Volatility Plays

Straddles and strangles help you profit from big price swings in either direction. A long straddle combines buying both a call and put with similar strike prices and expiration dates. You’ll use these when you expect big moves but aren’t sure which way the market will go. The strategy pays off when the underlying security moves past either breakeven point.

Strangles work much the same way but use different strike prices. You buy out-of-the-money calls and puts with matching expiration dates. This costs less than straddles but needs bigger price moves to make money. Both strategies can get hit hard by “volatility crush” after predicted events like earnings announcements.

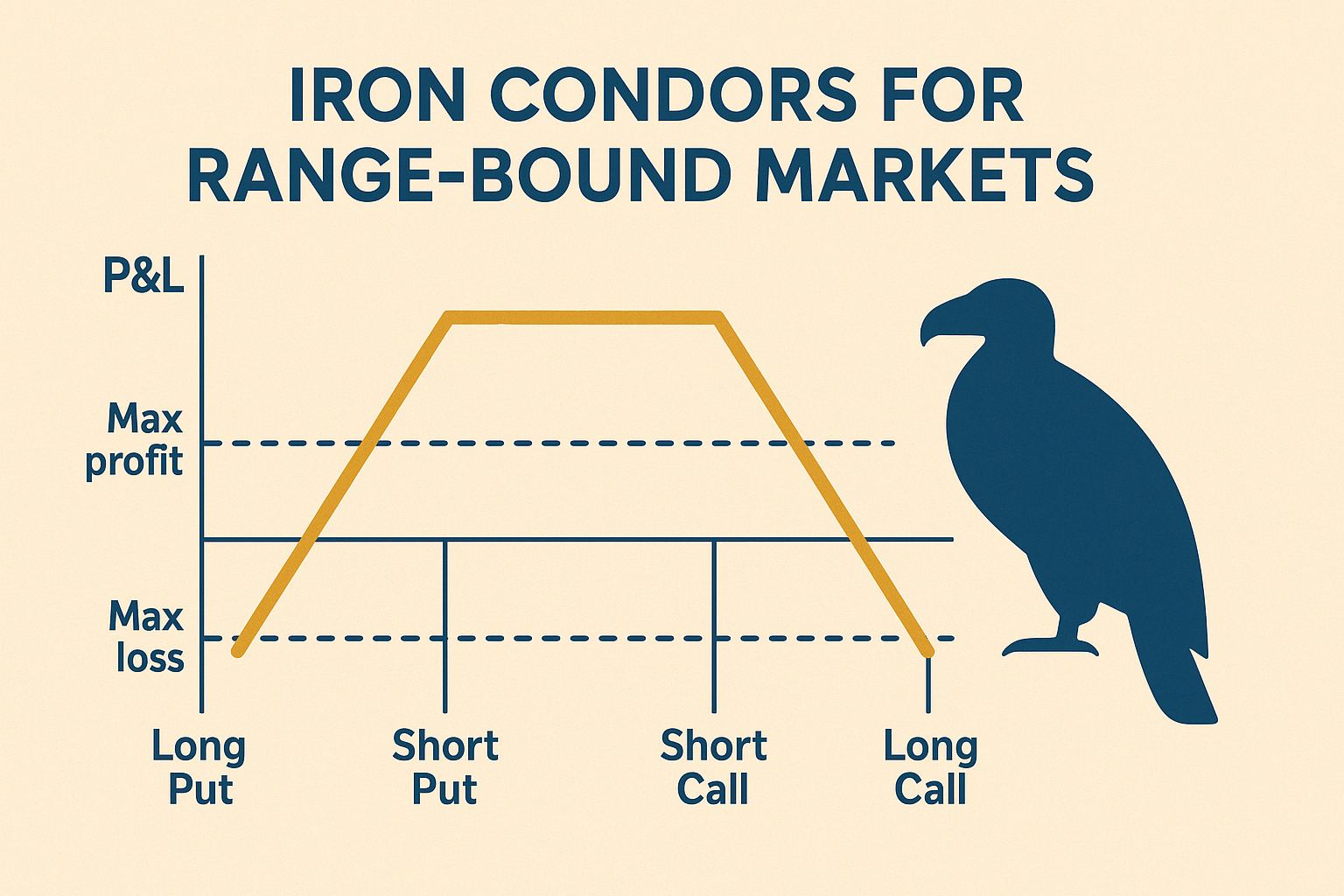

Iron Condors for Range-Bound Markets

Iron condors target markets that stay within a range and show low volatility. You sell an out-of-the-money put spread and call spread at the same time. This strategy uses four options that expire on the same date. Time decay works in your favor as long as the underlying asset stays between your short strikes.

The most you can make equals the upfront credit. Your maximum loss stays capped at the difference between either spread’s strikes minus what you collected in premium. You can also tweak the position to favor bullish or bearish moves by moving either spread closer to the current price.

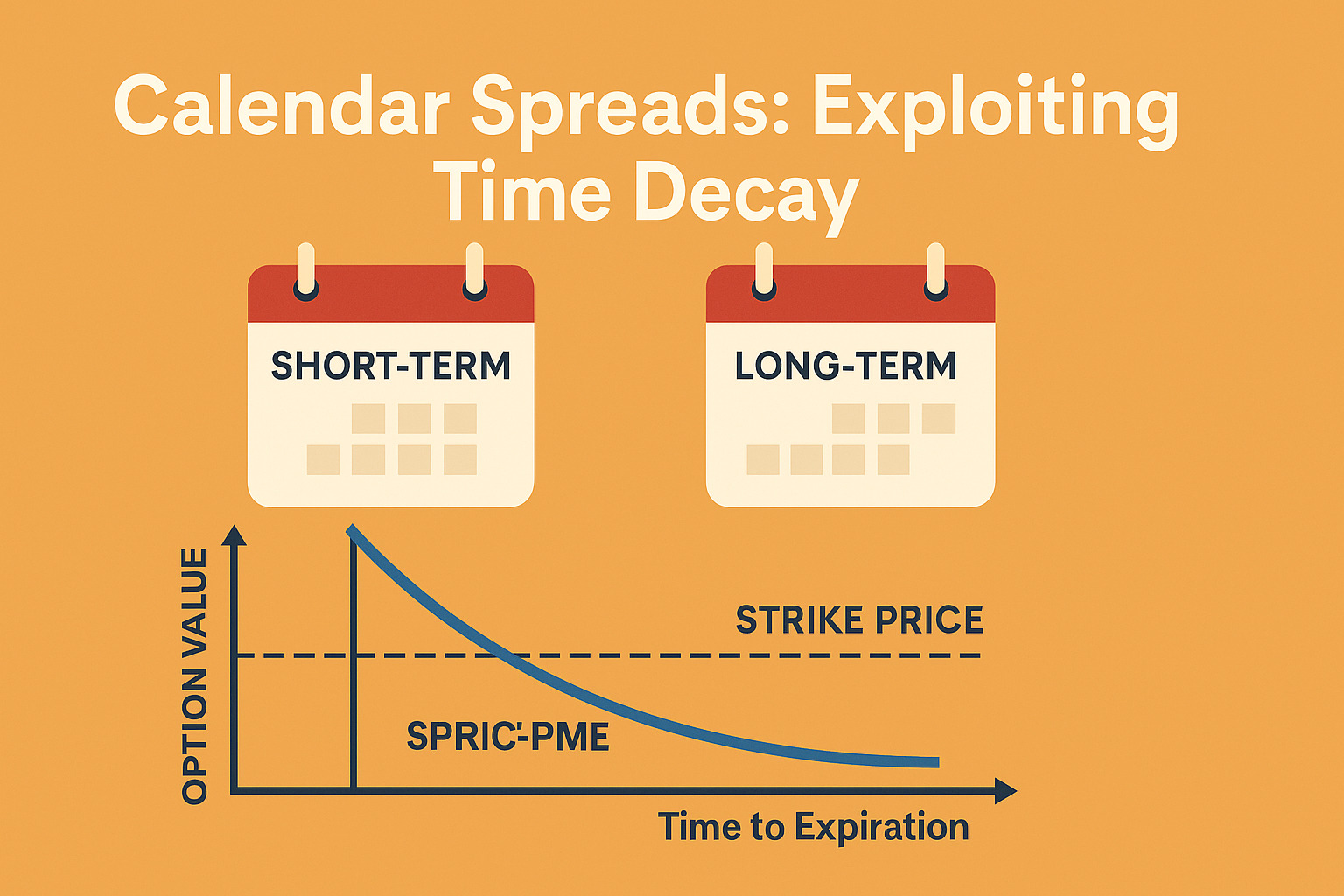

Calendar Spreads: Exploiting Time Decay

Calendar spreads mix selling short-term options with buying longer-term ones at the same strike price. This strategy takes advantage of how time decay works – shorter options lose value faster than longer ones.

These spreads work best when you think prices will stay steady until the near-term option expires, then move directionally later. They let you collect premium while keeping longer-term market exposure. If the price stays near the strike when the short option expires worthless, your long option still holds value.

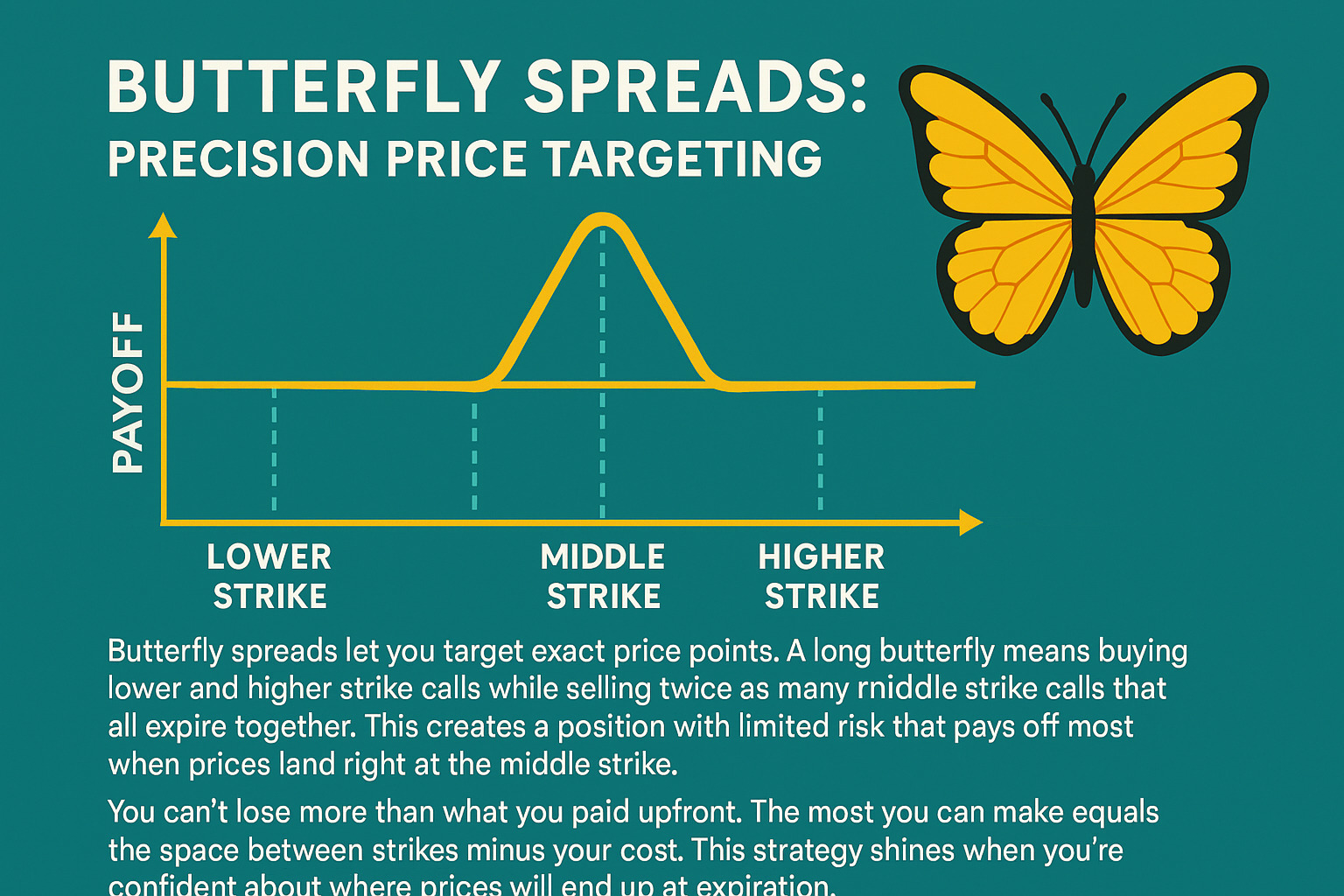

Butterfly Spreads: Precision Price Targeting

Butterfly spreads let you target exact price points. A long butterfly means buying lower and higher strike calls while selling twice as many middle strike calls that all expire together. This creates a position with limited risk that pays off most when prices land right at the middle strike.

You can’t lose more than what you paid upfront. The most you can make equals the space between strikes minus your cost. This strategy shines when you’re confident about where prices will end up at expiration.

Real-World Option Contract Examples

Real-life examples help us learn about option contracts and show how they work in different market situations.

Stock Option Contract Example with Profit/Loss Calculation

A plastic manufacturer’s story shows how options work in practice. The company worried about oil prices that sat at $25 per barrel. They feared prices might go above $30, so they bought a call option with a $30 strike price for a $1 premium. The manufacturer would only lose the $1 premium if oil prices stayed below $30. When prices jumped to $33, they used the option to buy at $30. This saved them $2 per barrel after counting the premium ($33 – $30 – $1). Their smart hedge limited losses while keeping the chance for bigger gains.

Index Option Contract Specifications

S&P 500 index options (SPX) use a $100 multiplier, which means each contract equals $100 times the index value. Strike prices come in steps of $5, $10, $25, $50, $100, and $200 based on when they expire. Nasdaq-100 index options (NDX) also use the $100 multiplier but work a bit differently. Their exercise prices come in $5 steps for contracts under $3 and $10 steps for those above. Both types follow European-style exercise rules, which only allow execution when they expire.

ETF Options Contract Case Study

Long-term equity anticipation securities (LEAPS) on defensive sector ETFs can diversify a tech-heavy portfolio. Investors cut their concentration risk by putting 25% of their funds into options on utilities, real estate, treasuries, and gold ETFs. This needed minimal capital. They picked options with 0.80 delta and January 2026 expiration to balance leverage and time decay effectively.

Commodity Options Contract Structure

Commodity futures options let you buy or sell specific futures contracts. Take a crude oil producer who wants protection from falling prices. They might buy a $60 put option to set a price floor. The option gets exercised if prices drop below $60. Higher prices mean they just lose the premium. Time plays a crucial role here – these options lose value as they get closer to expiration.

Risk Management Framework for Options Trading

Risk management is the life-blood of sustainable options trading that separates successful traders from those who quickly lose their account value. A well-laid-out approach to risk can protect your capital and create consistent growth opportunities.

Position Sizing and Capital Allocation

Position sizing serves as the basic building block of options risk management. Smart traders risk no more than 1-3% of their total capital on any single trade. You can calculate the right position size by:

- Determining your account risk (typically 2% of capital)

- Identifying your trade risk (distance between entry and stop-loss)

- Dividing account risk by trade risk to find position size

To name just one example, a $25,000 account with 2% risk tolerance means your maximum risk per trade equals $500. If you trade an option with $20 risk per contract, your position size calculation ($500/$20) shows 25 contracts maximum.

Greeks-Based Risk Monitoring

Option Greeks give you powerful metrics to monitor position risk. Delta-neutral strategies reduce directional risk by balancing positive and negative deltas close to zero. Gamma shows how quickly delta changes during price movements and warns you about potential volatility exposure. Positions with high gamma need smaller sizes and more active management.

High theta positions need careful attention to time decay effects, especially near expiration. Vega helps measure volatility risk—crucial during earnings announcements or economic events.

Adjustment Techniques for Existing Positions

Think about strategic adjustments rather than immediate exits when positions move against you. Rolling options—closing existing positions and opening new ones with different strikes or expirations—gives breathing room for challenged trades. You can reduce cost basis and risk exposure by selling offsetting options to create spreads.

Stock splits or mergers might require contract adjustments that change deliverables, strike prices, or contract multipliers.

Exit Strategies and Stop-Loss Implementation

Clear exit points remove emotion from trading decisions. Most traders use percentage-based exits—like a 50% loss or 100% gain threshold. OCO (one-cancels-other) orders let you place both stop-loss and profit-target orders at the same time.

Trailing stops adjust dynamically as positions gain value and help lock in profits while allowing continued upside. Technically-placed stops based on support/resistance levels or trendlines work better than arbitrary exit points.

Conclusion

Options contracts are powerful tools for hedging and speculation. But success requires deep understanding and disciplined execution.

This guide walks you through everything—from basic definitions to advanced multi-leg strategies.

Strike prices, expiration dates, and premiums form the core of every options trade. These elements shape your risk, potential profit, and overall strategy.

Standard contracts typically control 100 shares. However, this may change after events like stock splits or mergers.

Your strategy should match your goals. Use long calls in bullish markets or protective puts to guard against declines.

Advanced setups like iron condors and calendar spreads let you target specific market conditions with precision.

Risk management is key. Position sizing, tracking the Greeks, and setting exit rules help protect your capital and unlock growth.

Limit each trade’s risk to 1–3% of your total capital. And always plan adjustment strategies before exiting tough positions.

Options trading demands continuous learning. Start with the basics, build confidence, and grow your skillset over time for lasting success.

Frequently Asked Questions

1. What are the main types of option contracts?

There are two primary types of option contracts: call options and put options. Call options give the holder the right to buy an underlying asset at a predetermined price, while put options give the right to sell. Both have specific strike prices and expiration dates.

2. How is the value of an option contract calculated?

The value of an option contract is determined by its premium, which consists of intrinsic value and time value. Factors influencing the premium include the underlying asset’s price, strike price, time until expiration, market volatility, and interest rates.

3. Are all option contracts standardized to 100 shares?

While most standard option contracts represent 100 shares of the underlying asset, there are exceptions. Mini options may represent 10 shares, and corporate actions like stock splits can create non-standard contracts with different share quantities or unique deliverables.

4. What is the difference between American and European style options?

American-style options can be exercised at any time before expiration, offering maximum flexibility. European-style options, on the other hand, can only be exercised on the expiration date. This distinction affects option pricing and strategy implementation.

5. How can options be used for risk management?

Options can be powerful risk management tools. Protective puts can act as insurance for stock holdings, while covered calls can generate income and provide a small buffer against price declines. Additionally, various spread strategies can be employed to limit risk exposure while still participating in market movements.