Long Straddle Options: Proven Methods for Volatile Market Success

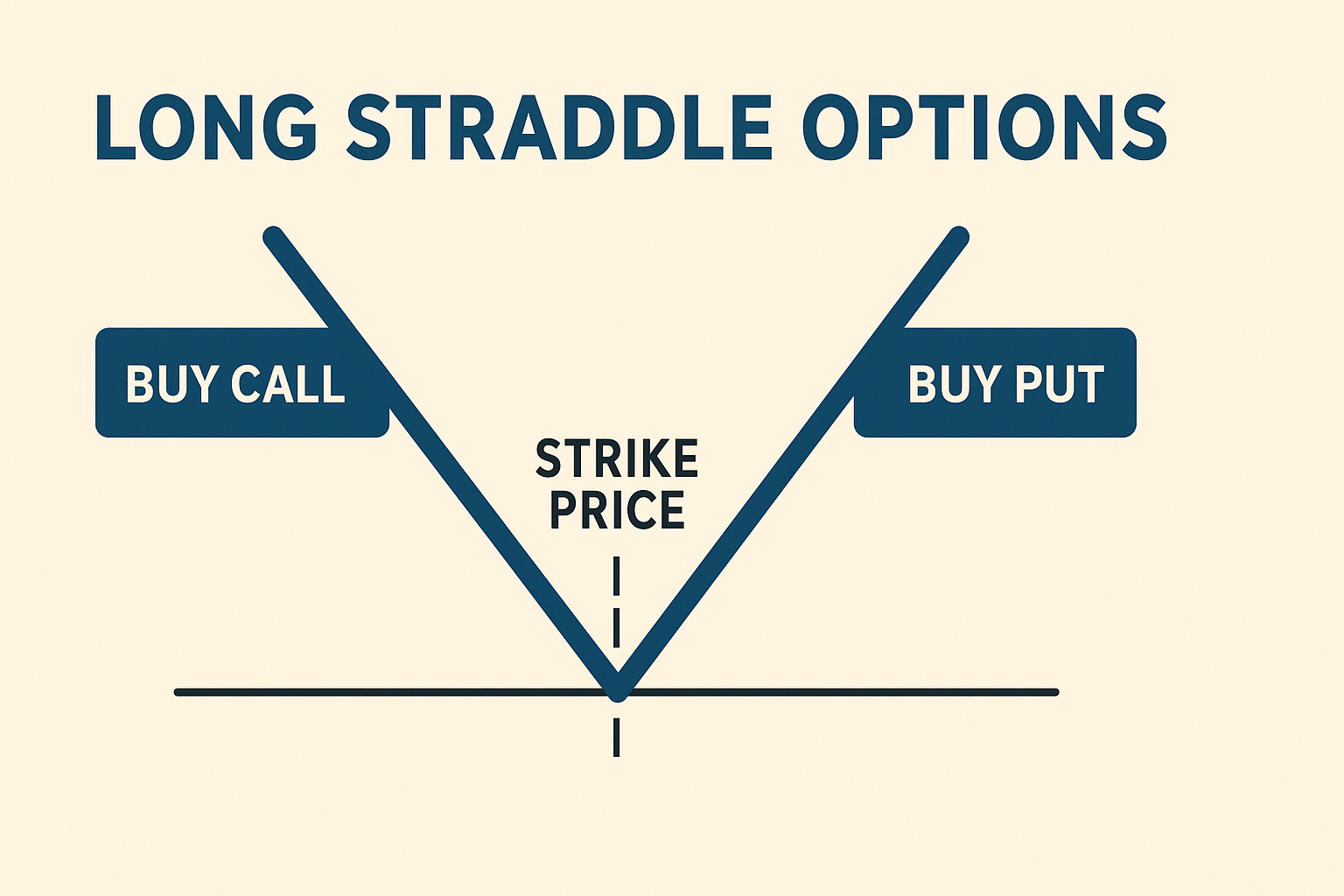

A long straddle is a market-neutral options strategy where a trader buys both a call and put option with the same strike price and expiration date. It profits from large price swings in either direction, with risk capped at the total premium paid and unlimited upside potential.

Want to profit from big market swings, no matter which way prices move? A long straddle gives you unlimited upside in either direction.

This strategy involves buying both a call and a put option on the same asset. Both options have the same strike price and expiration date.

Long straddles are ideal during high-volatility events. Think earnings reports, Fed decisions, or elections—times when markets move sharply.

Your maximum loss is limited to the total premium paid. That makes it a controlled way to trade unpredictable markets.

This guide teaches you how to build effective long straddle positions. You’ll learn when to use them, how to calculate breakeven points, and how they compare to other strategies.

Whether you’re experienced or just starting, long straddles can help you trade uncertainty with confidence.

- A long straddle involves buying a call and put option at the same strike price and expiration, benefiting from large price moves in either direction.

- The strategy profits from volatility, not direction, making it ideal before events like earnings or elections.

- Risk is limited to the total premium paid; profit potential is theoretically unlimited on the upside.

- Break-even points are strike price ± total premium; success depends on the underlying moving beyond either point before expiration.

- Advanced techniques like rolling, strike adjustment, and Greek analysis can improve outcomes in real market conditions.

What is a Long Straddle Option Strategy?

A long straddle is a powerful multi-leg options strategy that helps you profit from big price swings, whatever the market direction. You don’t need to guess which way the price will move. This neutral approach runs on volatility itself.

Core Components of a Long Straddle

The long straddle has two vital parts:

- A long call option purchase

- A long put option purchase

Both options must have similar characteristics: same underlying asset, same expiration date, and the same strike price. Traders usually pick at-the-money options with strike prices near the security’s current market value. This setup creates a position that stays neutral to direction but responds quickly to volatility.

You’ll need an upfront investment—a debit trade where you pay both options’ combined premium plus transaction costs. This original cost shows your maximum possible loss if things don’t go as planned.

How Long Straddles Profit from Volatility

Long straddles make money in two main ways:

Price Movement: You make profits when the underlying asset’s price moves by a lot in either direction past your break-even points. These points equal the strike price plus total premium paid (upper break-even) and strike price minus total premium paid (lower break-even). Moving beyond these points at expiration means profit.

Volatility Increases: The value of both options can go up together before expiration if implied volatility spikes sharply. This lets you exit with profits early. Long straddles work especially well before major market events like:

- Earnings announcements

- Federal Reserve decisions

- Product launches

- Regulatory approvals

- Election outcomes

Your profit potential has no limit on the upside and can be substantial on the downside (only limited because stock prices can’t go below zero). The bigger the price swing, the more money you can make.

Key Differences from Other Options Strategies

A long straddle is different from other volatility strategies in several ways:

Compared to Long Strangle: Both strategies bet on big price moves, but straddles use options with the same strike prices. Strangles use out-of-the-money options with different strikes (calls higher, puts lower). This means straddles give you:

- Closer break-even points

- Lower risk of total loss at expiration

- Less impact from time decay

- Higher original cost and maximum risk

Versus Directional Strategies: Bullish or bearish positions need you to predict the right direction. Long straddles are “directionally agnostic”. They make money from how much prices move, not which way they go. This makes them perfect when you expect volatility but aren’t sure about market direction.

The biggest advantage is having risk-defined exposure to volatility with unlimited profit potential. All the same, time decay can hurt you as both options lose value near expiration if the asset doesn’t move much. On top of that, implied volatility often rises before predicted events, which makes options more expensive to buy.

Setting Up Your First Long Straddle Trade

Your first long straddle setup needs careful planning and the right execution. Market conditions must be right for this strategy. Let’s look at the steps you need to take to set yourself up for success.

Selecting the Right Underlying Asset

The right underlying securities form the base of a working long straddle. Here’s what to look for in assets:

- Price movement patterns or chances of big price changes

- Events that could shake up prices, like earnings reports, product launches, or regulatory decisions

- Enough liquidity to move in and out of positions quickly

The best picks often show low current volatility but have triggers that could cause big price moves. This lets you buy options at better prices before volatility rises.

Determining Optimal Strike Price and Expiration

To make your long straddle work best:

Pick strike prices at-the-money (ATM) or as near as you can to the current market price. This creates a neutral position that profits from moves in either direction.

When picking expiration dates, weigh these factors:

- Options with longer terms give more time but cost more

- Short-term options cost less but need faster price moves

- Match expiration with market events or announcements

Most traders pick 14 to 42 days for event-based trades, though your outlook might need different timing.

Calculating Entry Costs and Break-Even Points

The total premium of both options contracts is your starting investment and the most you can lose.

Here’s how to find break-even points:

- Upper break-even = Strike price + Total premium paid

- Lower break-even = Strike price – Total premium paid

Let’s say you buy a straddle at $100 strike price for $10 total premium. Your break-even points would be $90 and $110. The underlying needs to move about 10% either way for you to profit.

Step-by-Step Trade Execution Process

- Check market conditions and pick a good underlying asset

- Pick expiration date based on expected catalysts

- Find the at-the-money strike price nearest to current market value

- Add up premium costs and check against your risk comfort level

- Size your position—seasoned traders put no more than 5% of their capital in one straddle

- Buy both put and call options at the same time

- Watch the position, especially price moves and implied volatility changes

Time decay hurts long straddles, so you need a clear exit plan. Smart traders set targets (like 40% gain) and loss limits to handle risk well.

Advanced Long Straddle Techniques for Experienced Traders

After you become skilled at simple long straddle implementation, you can use several advanced techniques to improve your results. Traders with experience know that active management of these positions leads to better outcomes than holding until expiration.

The Rolling Straddle Method

The rolling straddle technique gives your position a longer life when volatility doesn’t meet expectations. You can sell-to-close (STC) your current straddle and buy-to-open (BTO) a new position with a later expiration instead of taking a loss. This adjustment keeps your volatility exposure and resets time decay. You can also adjust the strike price to match any stock price changes since entry. Note that rolling usually needs additional premium, which increases your break-even points and maximum potential loss.

Combining with Other Positions

Smart traders often match long straddles with complementary strategies. They might combine long dated straddles with short-dated short straddles. This combination has shown good results by offsetting the long position’s time decay. You can also convert your long straddle to a reverse iron butterfly by selling options above and below your long strikes in declining volatility environments. This change reduces maximum loss but limits your profit potential.

Adjusting Strikes Based on Market Movement

Strategic adjustments become crucial when markets move against your long straddle position. Traders often use “legging in” techniques—they buy one side of the straddle first, then add the other component at better prices. If implied volatility rises but the underlying barely moves, you might want to take profits on both legs rather than wait for a price breakout.

Using Greeks to Optimize Entry Timing

Greeks give vital information about timing long straddle entries. Near-zero delta positions work best for pure volatility plays because they show minimal directional bias. Positive gamma brings value—your position’s delta becomes more positive as prices rise and more negative as prices fall. Vega sensitivity matters most since long straddles profit from volatility increases. The best time to enter is when implied volatility sits near historical lows but looks ready to rise, which creates a favorable risk-reward profile for your capital.

Note that advanced straddle techniques need active management. You shouldn’t use a passive approach. Good position sizing remains vital—even sophisticated strategies work better when you limit allocation to 5% of your available trading capital.

Managing Risk in Long Straddle Positions

You need robust risk control measures to execute a successful long straddle strategy. The profit potential has no theoretical limits, yet you must learn to manage and alleviate potential losses.

Maximum Loss Calculation and Management

The total premium paid for both options plus transaction costs defines your maximum risk in a long straddle. Both options expire worthless and create this worst-case scenario when the underlying asset’s price matches the strike price at expiration. To cite an instance, your maximum potential loss becomes $600 if you paid a combined premium of $600 for both call and put options.

This defined risk gives you a substantial advantage over many other trading strategies. The premium outlay can still be hefty since you’re buying two options instead of one.

Using Stop-Loss Orders Effectively

Stop-loss orders add another layer of protection to your long straddle positions. You should set predetermined exit points based on:

- A percentage of your original premium investment (e.g., exit if losing 50% of premium)

- Time-based factors (exit if price stays flat after a set period)

- Declining implied volatility indicators

Your capital stays better protected when you exit the trade before expiration, especially if the predicted price movement hasn’t happened and time decay speeds up.

Position Sizing for Long Straddles

Proper position sizing plays a crucial role with long straddles. You must limit your position’s size compared to your overall portfolio to control risk. Most experienced traders suggest putting no more than 5% of your trading capital into a single straddle position.

Note that market inefficiency makes straddle prices reliable indicators of likely price movements before expiration. Putting too much capital into one position could hurt your portfolio.

Hedging Techniques for Additional Protection

These hedging approaches offer extra protection:

- Roll up the long put to lock in gains while maintaining protection if the underlying moves up substantially

- The long call could roll down if the asset price falls

- Lock in partial profits early to reduce exposure while keeping some upside potential

Such adjustments protect you from sudden reversals and optimize your long straddle position’s risk-reward profile.

Proven Long Straddle Examples from Real Markets

The analysis of real-life examples shows how long straddles actually perform in markets of all types. These case studies tell us about the ups and downs traders face with this strategy.

Case Study: Earnings Announcement Straddle (2023)

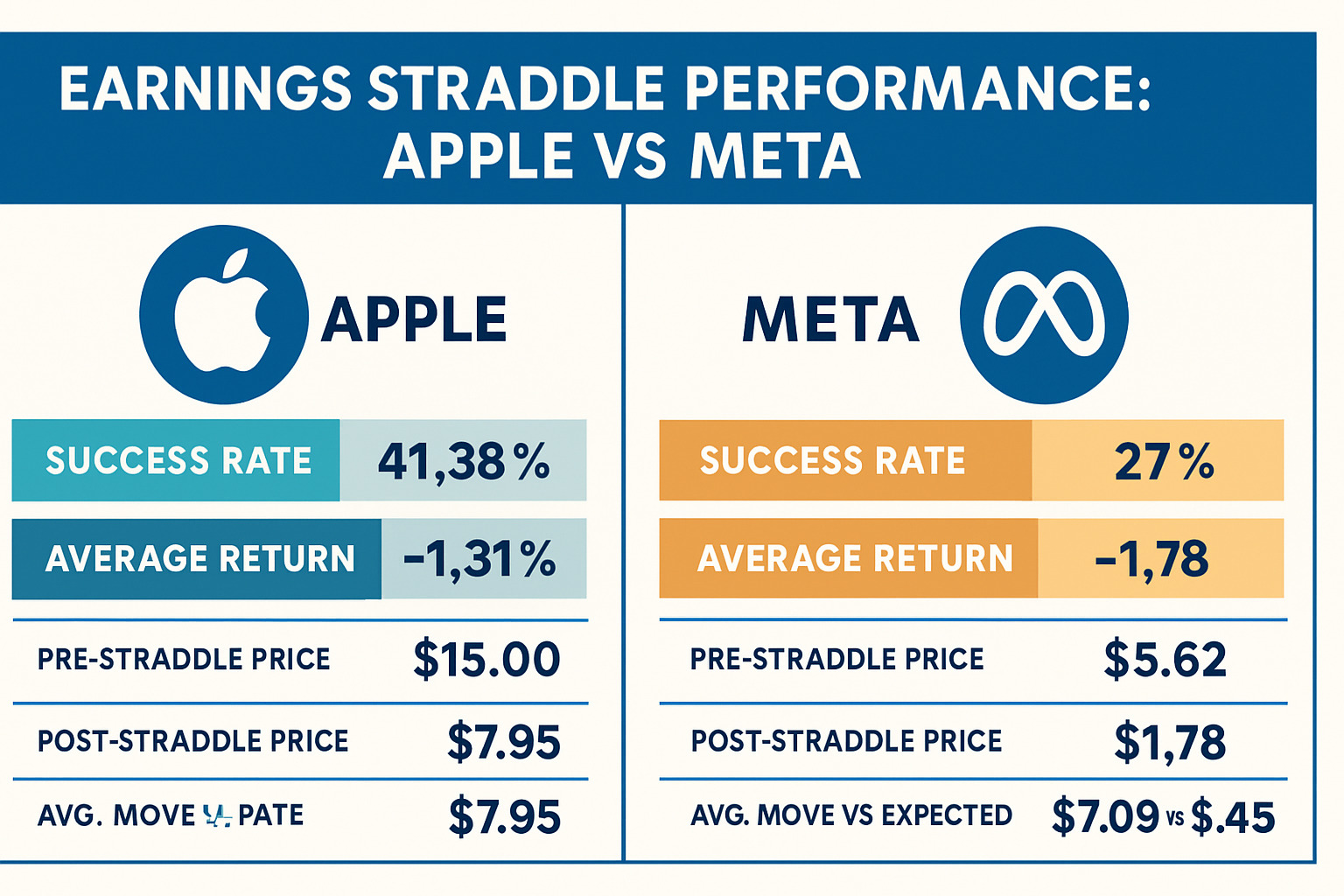

Apple’s earnings reports serve as perfect testing grounds for long straddle option strategies. Our largest longitudinal study of Apple straddles from 2007 through 2023 reveals these positions won only 41.38% of the time. The ten-year period showed an average return of -1.31%.

The market priced Apple’s pre-earnings straddles at $15.00, but they fell to $7.95 after earnings announcements. This volatility collapse, not the direction of price movement, determined whether traders made money.

Meta’s earnings straddles did even worse with success rates of just 27%. The pre-earnings straddle price of $5.62 dropped to $1.78 after announcements. The stock’s average move of $7.09 beat market expectations of $6.45.

Case Study: Market Uncertainty Straddle (2022)

Market uncertainty in 2022 created new ways to position straddles strategically. Ford’s case during economic concerns tells an interesting story. A trader’s long straddle with $12.00 strike price options (at $0.80 each) lost the full $1.60 premium per contract when the stock stayed at $12.00, even with strong sales numbers.

The same happened with Exxon during government shutdown fears. A straddle using $110 strike options at $5 each lost value when the stock barely moved to $112. The $10 premium investment ended in the red.

Performance Analysis and Key Takeaways

Chipotle straddles showed a win rate of just 35.48% with -2.59% average annual returns. The stock moved $5.28 on average, well below the expected $7.01.

Here’s what we learned:

- Volatility collapse happens after announcements, and long straddles lose money whatever the price does

- Market efficiency means straddle premiums usually reflect the expected move correctly

- Timing patterns exist—stocks beating expected moves often underperform next time

Traders need more than volatility predictions to succeed with long straddles. They must understand how options markets price expected moves and volatility behavior around big events.

Long Straddle vs Long Strangle: Strategic Differences

Long straddles and long strangles both aim to capture market volatility but take different paths to reach similar goals. These strategies might look alike at first glance, but vital differences determine which one works best in specific market conditions.

Cost Structure Comparison

The main difference between these strategies lies in their cost structure. Long straddles need at-the-money call and put options with similar strike prices, which leads to higher premiums. Long strangles work differently. They use out-of-the-money options with different strike prices and usually cost about half as much as comparable straddles. A straddle might cost $2.80 ($1.40 call + $1.40 put), while a similar strangle could cost just $1.40. Traders can buy more strangle positions with the same money because of this price difference, which might increase their overall exposure to volatility.

Risk-Reward Profile Analysis

These strategies show different risk-reward profiles in several ways. Long straddles have closer break-even points that make it easier to turn a profit with smaller price movements. They also hold up better against time decay and are less likely to lose all premium at expiration. Long strangles need bigger price swings to become profitable because their break-even points are further apart. A strangle’s wider spread between strike prices creates a bigger “zone of maximum loss” where both options might expire worthless if the underlying asset stays between the strike prices.

When to Choose a Straddle Over a Strangle

A long straddle makes sense when you:

- Want to tap into significant volatility but need closer break-even points

- Worry about time decay eating into your position value

- Need less risk of complete loss at expiration

- Think moderate price movement could happen either way

A long strangle works better when you:

- Want to preserve capital while still getting volatility exposure

- Expect very large price movements that will clear wider break-even points

- Plan to set up multiple positions with limited capital

Converting Between Strategies Mid-Position

Market conditions often lead traders to switch between these strategies. You can turn a straddle into a strangle by rolling one leg to a different strike price. This change widens your position’s profit zone and reduces capital at risk. The trade-off brings wider break-even points and a higher chance of maximum loss if price movement falls short.

Conclusion

Long straddle options are a great way to get profits from market volatility no matter which direction the market moves. This strategy works best when traders analyze ground examples carefully and manage their risks well.

Your success with long straddles just needs you to focus on these key elements:

- Pick the right assets that could show volatility

- Work out exact break-even points and know your maximum risk

- Take an active approach to position management instead of waiting for expiration

- Keep position sizes small to protect your trading funds

The market data shows mixed outcomes for long straddles, especially when you have earnings seasons. The profit potential has no upper limit in theory. Your actual returns depend on your timing and how well you assess volatility. Traders often find that their biggest challenge comes from sudden drops in volatility after major market events.

This knowledge helps you trade long straddles more strategically. Note that you need to balance the higher premium costs against possible returns while keeping tight risk controls. Long straddles cost more than long strangles but give you closer break-even points. They also handle time decay better, which makes them valuable tools in specific market situations.

Frequently Asked Questions

1. How does a long straddle strategy profit from market volatility?

A long straddle profits from significant price movements in either direction. As volatility increases, both the call and put options in the straddle tend to rise in value, potentially leading to profits. The strategy is particularly effective before major market events that could cause substantial price swings.

2. What are the key components of a long straddle option strategy?

A long straddle consists of buying both a call and a put option with identical strike prices and expiration dates on the same underlying asset. This structure allows traders to benefit from price movements in either direction while limiting the maximum loss to the total premium paid for both options.

3. How do you calculate the break-even points for a long straddle?

To calculate the break-even points for a long straddle, add the total premium paid to the strike price for the upper break-even point, and subtract the total premium from the strike price for the lower break-even point. The underlying asset’s price must move beyond these points for the strategy to become profitable.

4. What are the main risks associated with long straddle positions?

The primary risks of long straddles include the potential loss of the entire premium paid if the underlying asset’s price doesn’t move significantly, and the negative impact of time decay on the options’ value. Additionally, a decrease in implied volatility can reduce the value of both options, potentially leading to losses.

5. How does a long straddle compare to a long strangle strategy?

While both strategies aim to profit from volatility, long straddles use at-the-money options with identical strike prices, resulting in higher premiums but closer break-even points. Long strangles use out-of-the-money options with different strike prices, costing less but requiring larger price movements to become profitable. Straddles are generally less sensitive to time decay and have a lower risk of complete loss at expiration.